Step 1: Find Out What Plans Are Available at Your School

Start by asking your HR department or benefits coordinator:

- “Does our district offer a 403(b), 457(b), or both?”

- “Do we have an approved vendor list?”

- “Is there an employer match?”

Many school districts offer both plans, but you’ll need to go through approved providers.

Pro Tip: Ask for a brochure or a link to your district’s retirement plan website.

Step 2: Get the Vendor List (and Avoid the Bad Ones)

Once you know what plans are offered, your district will give you a list of approved vendors (investment companies). Unfortunately, not all vendors are created equal.

You want to look for:

- Low fees

- Index fund options

- No surrender charges or sales commissions

💡 Some well-regarded options (if available):

- Fidelity

- Vanguard

- Aspire

- TIAA

🚩 Watch out for high-fee annuities or salespeople pushing products you don’t understand.

Step 3: Open Your Account with the Vendor You Choose

Once you’ve picked a vendor:

- Visit their website or call their support line.

- Open a 403(b) and/or 457(b) account as a public school employee.

- Choose your investment options (I’ll cover the simplest way to choose funds in a future post — but for now, look for “Target Date” or “S&P 500 Index” funds if you’re unsure).

What Is a Target Date Fund?

A target date fund is a type of mutual fund that automatically adjusts its investment mix over time based on the year you plan to retire.

Simple definition:

It’s a “set-it-and-forget-it” investment that starts out aggressive and becomes more conservative as you get closer to retirement.

🔧 How It Works

Let’s say you’re planning to retire in 2045. You’d choose a fund like:

- Vanguard Target Retirement 2045 Fund (VTIVX)

- Fidelity Freedom 2045 Fund (FFFGX)

That fund will:

- Start out aggressive — with more stocks (which grow faster but are riskier)

- Slowly shift toward more bonds and stable investments as the year 2045 approaches

I’m not telling you to pick these exact funds, these are for example purposes. Ask the vendor that you choose what their Target Date Fund names are. If it’s 2025, and you want to retire in 2050, you will pick a 2050 Target Date fund.

Please keep in mind that you don’t have to choose a Target Date fund. However, you will want to work with the vendor or your representative on which mutual fund to choose.

Step 4: Submit a Salary Reduction Agreement with your HR department.

Opening the account is only half the process — now you need to fund it.

Ask HR for a Salary Reduction Agreement form. This is what allows money to be taken directly from your paycheck into your retirement plan. Some vendors have representatives that help you with all of the paperwork.

Fill it out and choose how much to contribute — even $50 a paycheck is a great start. This is the amount that I started with and eventually increased it. Keep in mind that even though you are deducting $50 a paycheck, your paycheck will likely not decrease by $50 but rather a smaller amount since this is “pre tax money”. Depending on your tax bracket, you might only see a $35 or $40 deduction in your paycheck.

Step 5: Start Small, Then Grow

Once you’re contributing, you’re on the path. Increase your contributions slowly over time.

Examples:

- Try to start with a paycheck or $100 a paycheck or per month and then add to it once you figure out how much you can invest every month. In a future post, I will talk about ways that you can keep increasing it

- Add $25 or another amount every semester or every raise that you receive

- Work towards adding as much as you are comfortable with. Keep in mind the max is $23,500/year for 2025 in each plan. If someone is 50 or older, the max is $31,000.

Real World Example of how much to invest to reach a certain goal:

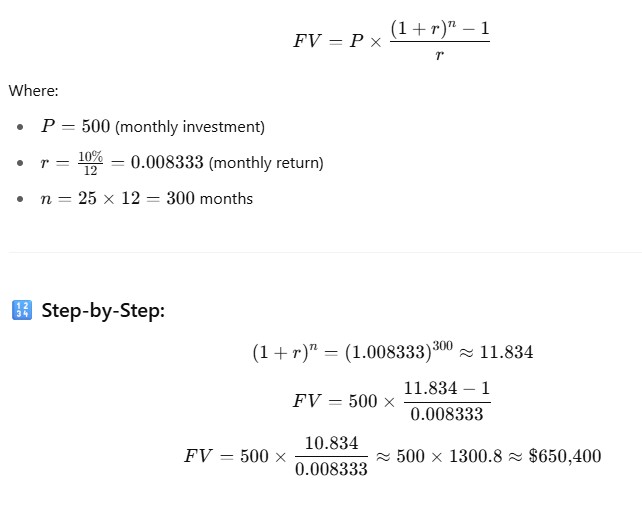

Let’s say you are 30 years old and you would like to retire by 55 years old and supplement your pension with your investment accounts (403b or 457b or both). Let’s say your goal is to accumulate at least $650,000 in 25 years. Assuming 10% average interest per year, you will need $500 per month in order to reach this goal.

Formula Used:

Why did I choose 10% interest for this example? It’s just a guess based on the past history of the performance of the stock market (S&P 500).

From 2014 to 2024, the S&P 500 delivered robust returns, reflecting a period of significant market growth. Here’s a breakdown of the annual performance:

| Year | Total Return |

|---|---|

| 2014 | 13.69% |

| 2015 | 1.38% |

| 2016 | 11.96% |

| 2017 | 21.83% |

| 2018 | -4.38% |

| 2019 | 31.49% |

| 2020 | 18.40% |

| 2021 | 28.71% |

| 2022 | -18.11% |

| 2023 | 26.29% |

| 2024 | 25.02% |

Over this decade, the S&P 500 achieved a cumulative total return of approximately $364.37 for every $100 invested at the beginning of 2014, assuming dividends were reinvested. This equates to an average annual return of about 13.22%.

The average annual return of the S&P 500 over the last 40 years (roughly from 1984 to 2024) is approximately 11-12%, including dividends reinvested.

Here’s why:

- Historically, the S&P 500 has averaged about 10% per year over the very long term (since its inception).

- Over recent decades, especially the last 40 years, the return is often cited closer to 11-12%, thanks to periods of strong growth like the 1980s and 1990s bull markets, along with reinvested dividends.

Sources:

Keep in mind, returns vary widely year to year, and past performance doesn’t guarantee future results.

Morningstar, Vanguard, and other financial research generally support this 11-12% figure when dividends are included.

Use my retirement calculator below to customize this for your own goals based on what you can afford to invest per month.

Leave a Reply