Not all teachers in the United States automatically have access to a 403(b) or 457(b) retirement plan — it depends on a few key factors like employer, school district, and state.

June 7, 2025

Note: This is based on information as of June of 2025. Contributions limits usually change each year. Please check with your accountant and read the Disclaimer:

Here’s a breakdown:

✅ 403(b) Plans

- Most public school teachers are eligible.

- These are offered by public schools, certain nonprofits, and some charter schools.

- If you’re a teacher in a public K–12 school, there’s a very high chance you have access to a 403(b).

- Private school teachers may also be eligible if their school is a qualifying nonprofit (501(c)(3)).

📌 Bottom line:

Nearly all public school teachers have access to a 403(b), but not all private or charter school teachers do.

✅ 457(b) Plans

- These are typically offered by state and local governments.

- Many public school districts also offer a 457(b), especially in larger or better-funded districts.

- However, 457(b) access is less universal than 403(b) — some districts don’t offer it at all.

📌 Bottom line:

Many public school teachers do have access to a 457(b), but it’s not guaranteed — and it’s less common than the 403(b).

🏫 Summary by Type of School

| School Type | 403(b) Likely? | 457(b) Likely? |

|---|---|---|

| Public School | ✅ Yes | ✅ Maybe |

| Charter School | 🟡 Sometimes | 🟡 Rarely |

| Private School (nonprofit) | ✅ Often | ❌ Rarely |

| Private School (for-profit) | ❌ Unlikely | ❌ Unlikely |

So, what do you do if you work for a school that doesn’t offer a 403b or 457b?

If you’re a teacher without access to a 403(b) or 457(b) — whether you’re at a private school, charter school, or a small institution — you’re not stuck. You can still build a strong retirement plan using individual retirement accounts (IRAs) and potentially other options, depending on your full situation.

🧭 Here’s What a Teacher Without a 403(b)/457(b) Can Do:

✅ 1. Open an IRA (Individual Retirement Account)

This is the best starting point for most people who don’t have an employer plan.

✳️ Two types to choose from:

| IRA Type | Contributions | Tax Benefit | Best For |

|---|---|---|---|

| Roth IRA | After-tax money | Tax-free withdrawals in retirement | Younger teachers, or anyone expecting to be in a higher tax bracket later |

| Traditional IRA | Pre-tax (if eligible) | Tax deduction now; taxed later | People who want a tax break this year |

💵 2024 IRA limits:

- $7,000 per year

- $8,000 if you’re age 50+

You can open an IRA for free through:

✅ 2. Contribute to a Taxable Brokerage Account

After maxing your IRA, invest extra savings in a brokerage account.

- No tax benefits, but no limits

- Fully flexible — use the money whenever

- Still lets you invest in the stock market, ETFs, index funds, etc.

Great for:

- Early retirement

- Supplemental savings

- Teachers planning for sabbaticals or a second career

✅ 3. Solo 401(k) (Only if you have side income)

If you earn any freelance or side income (tutoring, summer programs, curriculum writing, etc.), you qualify for a Solo 401(k) or SEP IRA — which allow you to save a lot more.

| Account | Max Contribution (2024) | Best For |

|---|---|---|

| Solo 401(k) | Up to $69,000 | Teachers with side gigs or small businesses |

| SEP IRA | Up to 25% of net income | Similar use, easier to manage |

✅ 4. Ask Your School to Add a Plan (if possible)

If you work for a nonprofit private school, they’re eligible to offer a 403(b) — they just might not have done it yet.

- Get other teachers interested

- Talk to HR or administration

- Suggest providers like TIAA, Vanguard, or Fidelity 403(b)

🧠 Summary: What You Can Use Without a 403(b)/457(b)

| Option | Tax Benefit | Contribution Limit | Notes |

|---|---|---|---|

| Roth IRA / Traditional IRA | ✅ Yes | $7,000 ($8,000 age 50+) | Great starting point |

| Taxable Brokerage Account | ❌ No | Unlimited | Flexible, no penalties |

| Solo 401(k) or SEP IRA | ✅ Yes | Up to $69,000 | If you have side income |

Can a teacher save money in a Roth IRA and a traditional IRA?

a teacher can save money in both a Roth IRA and a Traditional IRA in the same year, but there’s a combined contribution limit between the two.

✅ Here’s How It Works:

🏦 2024 IRA Contribution Limits

- Total combined contribution limit:

👉 $7,000 (or $8,000 if you’re age 50+) - You can split this amount between a Roth IRA and a Traditional IRA however you like.

🔄 Example Scenarios

| Roth IRA | Traditional IRA | Total |

|---|---|---|

| $7,000 | $0 | ✅ OK |

| $3,500 | $3,500 | ✅ OK |

| $1,000 | $6,000 | ✅ OK |

| $7,000 | $1,000 | ❌ Too much (exceeds limit) |

⚠️ Income Limits Matter for Roth IRA Contributions

You can always contribute to a Traditional IRA, but whether your Roth contributions (or Traditional IRA tax deduction) are allowed depends on your modified adjusted gross income (MAGI).

🧾 2024 Roth IRA income limits:

| Filing Status | Full Roth Contribution | Phased Out | Not Eligible |

|---|---|---|---|

| Single | < $146,000 | $146k–161k | > $161,000 |

| Married Joint | < $230,000 | $230k–240k | > $240,000 |

If you’re under these income limits, you can contribute the full $7,000 to a Roth.

💡 Why Use Both?

You might choose to split your contributions if you:

- Want to diversify your tax exposure in retirement

- Expect your income to rise significantly in future years

- Aren’t sure whether your tax rate in retirement will be higher or lower

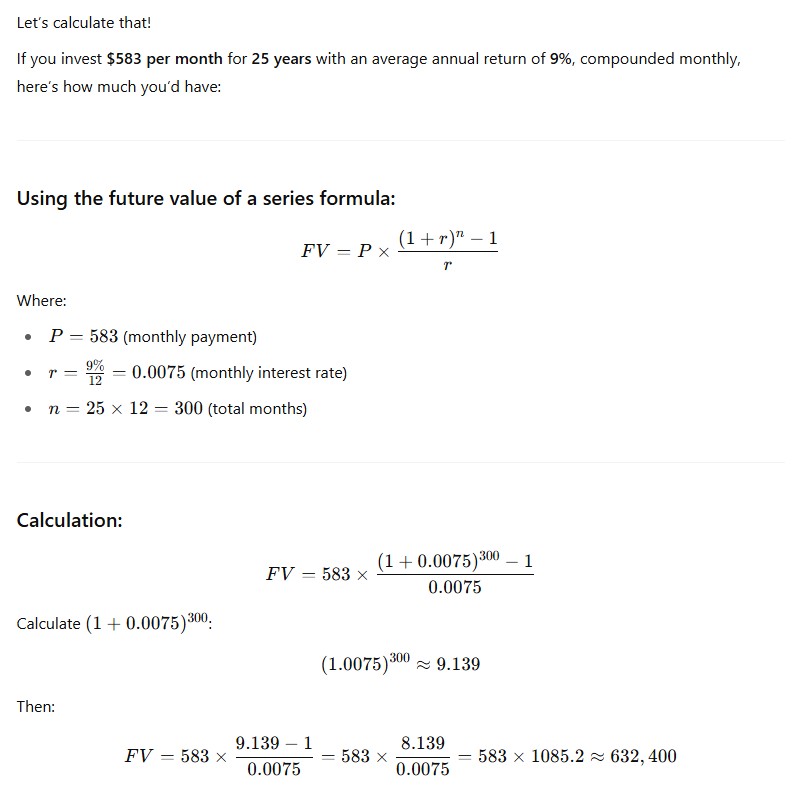

It’s important to note that even if you are restricted to only being able to invest $7000 a year into a Traditional IRA, that equates to $583 a month. If you were to invest this amount every month for 25 years and assumed a 9% return each year, you would end up with $632,400 after 25 years.

Here is how that was calculated: